| Table A: Average Effective Carbon Rate on Selected Fuels, 2014-2018 | |||||

| € per tonne of carbon dioxide emitted | |||||

| Fuel | 2014 | 2015 | 2016 | 2017 | 2018 |

| Petrol | 255.88 | 256.99 | 255.97 | 238.99 | 257.93 |

| Autodiesel | 180.72 | 182.96 | 183.88 | 171.88 | 183.92 |

| Jet Kerosene | 0.11 | 0.10 | 0.12 | 0.10 | 0.10 |

| Aviation Gasoline | 204.08 | 215.09 | 214.61 | 211.56 | 209.56 |

| Residual Fuel Oil for Maritime Transport | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Marked Gas Oil for Agriculture and Fishing | 37.18 | 36.90 | 37.02 | 37.08 | 39.44 |

| Household Heating Fuels | 22.39 | 23.71 | 24.52 | 24.10 | 24.58 |

| Fuels used in Industry | 6.99 | 6.81 | 6.71 | 6.70 | 6.73 |

| Fuels used in Electricity Generation | 3.22 | 3.04 | 2.86 | 3.11 | 3.56 |

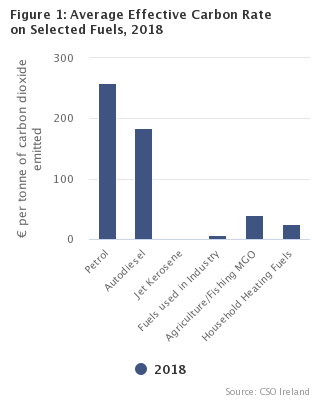

In 2018, consumers of petrol paid on average €257.93 per tonne of carbon dioxide emitted, while carbon dioxide emissions from jet kerosene were effectively charged at €0.10 per tonne on average (see Table A and Figure 1). The average effective carbon rate on autodiesel was €183.92 in 2018.

|

The average effective carbon rate of a fuel is defined as net energy tax receipts divided by total tonnes of carbon dioxide emitted through combustion of the fuel. The energy taxes included are Excise Duty, Carbon Tax, Electricity Tax, the National Oil Reserves Agency (NORA) Levy, the Public Service Obligation (PSO) Levy and emission permit purchases under the EU Emissions Trading Scheme. |

Petrol had the highest average effective carbon rate each year from 2000-2018 (see Table 1). Petrol consumption is subject to the highest rate of Excise Duty, and is also subject to Carbon Tax and the NORA Levy. The rate of Excise Duty (inclusive of Carbon Tax) on petrol was used as the benchmark rate for fuels used in transport and industry in calculations of fossil fuel subsidies due to revenue foregone in this release.

The lowest average effective carbon rates were on residual fuel oil used for maritime transport and jet kerosene used in aviation. This was because fuel consumption for international maritime transport and international aviation is exempt from Excise Duty, Carbon Tax and the NORA Levy. In 2018, energy taxes were paid on less than 1% of fuel used for water and air transport. In contrast, energy taxes were paid on 100% of petrol consumption.

The electricity generation sector is exempt from Carbon Tax and Excise Duty but participates in the EU Emissions Trading Scheme (ETS). The average effective carbon rate on carbon dioxide emissions under the ETS was lower than the Carbon Tax each year since the Carbon Tax was introduced. In 2018 the average effective carbon rate for the electricity generation sector was €3.56 per tonne of carbon dioxide emitted.

Average effective carbon rates for 2000-2018 are shown in Table 1, with a breakdown by sector and type of fuel.

In 2018, €2.4 billion in direct subsidies and revenue foregone due to preferential tax treatment supported fossil fuel activities in Ireland (see Table 2). This was an increase of 8% on 2017.

Fossil fuel subsidies can support either production or consumption activities. In Ireland, subsidies to fossil fuel producers include zero royalty payments on gas and oil production, which were €91 million in 2018. Subsidies to consumers include the PSO Levy support to electricity generation from peat, which was €66 million in 2018 and revenue foregone due to the excise duty exemption for jet kerosene used for domestic and international commercial aviation, which was €626 million in 2018.

|

The OECD defines a subsidy as the result of a government action that confers an advantage on consumers or producers, in order to supplement their income or lower their costs. This definition includes tax expenditures such as tax rebates, tax repayments and reduced tax rates, as well as direct subsidies. Tax expenditures are estimated using the revenue foregone method, which is described in the Background Notes. A subsidy is a fossil fuel subsidy if it is likely to incentivise fossil fuel activities. Fossil fuel activities include exploration, extraction, manufacturing, refining and distribution of fossil fuels on the production side, as well as research and development supporting any of the above. Fossil fuel consumption by all sectors of the economy is also fossil fuel activity. |

Figure 2 shows direct and indirect fossil fuel subsidies from 2000-2018. Direct subsidies accounted for 12% of the support provided to fossil fuel activities in 2018, while tax repayments and other tax expenditures made up 88%.

| Year | Direct Subsidies | Indirect Subsidies |

|---|---|---|

| 2000 | 0.07922829699 | 1.340447087 |

| 2001 | 0.08153614019 | 1.42217950793 |

| 2002 | 0.1007486184 | 1.49448700528 |

| 2003 | 0.1490801497 | 1.35484695581566 |

| 2004 | 0.18786132125 | 1.56986367179613 |

| 2005 | 0.23178553109 | 1.99565490228285 |

| 2006 | 0.22504700066 | 2.09949232149023 |

| 2007 | 0.19993726549 | 2.02591994174941 |

| 2008 | 0.22484662658 | 2.17056208290023 |

| 2009 | 0.34816763837 | 1.73715867856 |

| 2010 | 0.35675816734 | 1.78546526832 |

| 2011 | 0.34068827637 | 1.70218550865 |

| 2012 | 0.3890637701 | 1.61379483606 |

| 2013 | 0.39068046269 | 1.54191063532 |

| 2014 | 0.45567711324 | 1.61076521974 |

| 2015 | 0.39028952935 | 1.72384789928262 |

| 2016 | 0.3518524479 | 1.73669547276711 |

| 2017 | 0.35429458139 | 1.88410014551271 |

| 2018 | 0.299645081 | 2.12391576211207 |

Figure 3 shows a comparison of the amount raised in energy taxes with expenditure on fossil fuel subsidies and expenditure on environmental subsidies aimed at protecting the air and climate, and reducing fossil fuel use.

In 2018, €3.2 billion was raised in energy taxes, €0.5 billion was spent on environmental subsidies related to energy and emissions, and fossil fuel subsidies were €2.4 billion.

| Energy Taxes | Environmental Subsidies (Energy and Emissions) | Fossil Fuel Subsidies | |

| 2000 | 1.491339 | 0.000493 | 1.41967538399 |

| 2001 | 1.435771 | 0.00075645 | 1.50371564812 |

| 2002 | 1.674053 | 0.00335384 | 1.59523562368 |

| 2003 | 1.762909 | 0.01320775 | 1.50392710551566 |

| 2004 | 2.083833 | 0.02309842 | 1.75772499304613 |

| 2005 | 2.212724 | 0.02189842 | 2.22744043337285 |

| 2006 | 2.247115 | 0.01838994 | 2.32453932215023 |

| 2007 | 2.25111 | 0.05578681 | 2.22585720723941 |

| 2008 | 2.250213 | 0.06979132 | 2.39540870948023 |

| 2009 | 2.267246299 | 0.05849387 | 2.08532631693 |

| 2010 | 2.52048882499997 | 0.18407957 | 2.14222343566 |

| 2011 | 2.691957596 | 0.1659018 | 2.04287378502 |

| 2012 | 2.634405171 | 0.11332665 | 2.00285860616 |

| 2013 | 2.72134076559478 | 0.1171187 | 1.93259109801 |

| 2014 | 2.84019626999992 | 0.14122239 | 2.06644233298 |

| 2015 | 3.042883324 | 0.19909265 | 2.11413742863262 |

| 2016 | 3.13525459166667 | 0.29584528 | 2.08854792066711 |

| 2017 | 3.25800358066667 | 0.41174058 | 2.23839472690271 |

| 2018 | 3.17604088633333 | 0.54697738 | 2.42356084311207 |

| Table 1: Average Effective Carbon Rate by Sector and Type of Fuel, 2000-2018 | |||||||||||||||||||

| € per tonne of carbon dioxide emitted | |||||||||||||||||||

| Average Effective Carbon Rate | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| Road Transport Fuels | 140.55 | 120.97 | 140.46 | 145.87 | 160.96 | 160.16 | 159.87 | 159.00 | 160.73 | 181.78 | 199.14 | 206.73 | 210.11 | 208.84 | 204.23 | 204.04 | 202.55 | 187.58 | 199.52 |

| Petrol | 163.26 | 153.32 | 174.46 | 175.05 | 192.10 | 191.92 | 191.21 | 191.94 | 196.62 | 224.11 | 238.70 | 252.54 | 257.43 | 257.22 | 255.88 | 256.99 | 255.97 | 238.99 | 257.93 |

| Autodiesel | 120.49 | 93.76 | 112.45 | 122.30 | 136.50 | 135.88 | 137.31 | 136.30 | 136.16 | 152.82 | 172.98 | 178.07 | 182.97 | 184.04 | 180.72 | 182.96 | 183.88 | 171.88 | 183.92 |

| LPG | 52.77 | 33.65 | 30.41 | 30.50 | 28.21 | 35.82 | 40.26 | 40.53 | 39.37 | 37.47 | 47.63 | 53.37 | 58.54 | 61.26 | 60.73 | 61.56 | 61.82 | 59.20 | 59.53 |

| Aviation Fuels | 0.65 | 0.46 | 0.46 | 0.54 | 0.63 | 0.60 | 0.59 | 0.54 | 0.52 | 0.65 | 0.61 | 0.46 | 0.41 | 0.40 | 0.32 | 0.30 | 0.32 | 0.26 | 0.22 |

| Jet Kerosene | 0.47 | 0.30 | 0.31 | 0.36 | 0.41 | 0.43 | 0.43 | 0.38 | 0.38 | 0.44 | 0.37 | 0.20 | 0.14 | 0.13 | 0.11 | 0.10 | 0.12 | 0.10 | 0.10 |

| Aviation Gasoline | 78.52 | 79.53 | 88.49 | 91.33 | 100.72 | 100.02 | 100.99 | 101.22 | 100.11 | 185.36 | 201.48 | 212.97 | 215.53 | 210.16 | 204.08 | 215.09 | 214.61 | 211.56 | 209.56 |

| Rail Transport Fuels | 18.65 | 18.77 | 18.62 | 25.71 | 35.15 | 41.20 | 26.52 | 17.85 | 27.65 | 21.13 | 38.48 | 40.73 | 39.58 | 41.50 | 43.44 | 45.12 | 44.59 | 46.17 | 46.53 |

| Diesel | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 25.10 | 45.57 | 45.57 | 45.57 | 45.57 | 45.57 | 45.57 | 45.57 | 45.57 | 45.57 |

| Electricity | 0.00 | 0.00 | 0.00 | 5.11 | 8.24 | 8.93 | 3.74 | 0.00 | 4.13 | 0.96 | 4.25 | 14.46 | 10.25 | 17.55 | 30.87 | 42.69 | 39.63 | 49.56 | 52.99 |

| Water Transport Fuels | 1.18 | 1.31 | 1.65 | 1.60 | 2.32 | 2.80 | 3.36 | 3.13 | 4.22 | 3.47 | 6.04 | 6.48 | 5.97 | 5.39 | 6.62 | 5.85 | 6.66 | 6.23 | 6.49 |

| Marine Diesel | 1.49 | 1.62 | 2.32 | 2.30 | 3.04 | 3.32 | 4.40 | 5.05 | 6.36 | 4.35 | 7.49 | 7.53 | 6.86 | 5.94 | 7.36 | 6.24 | 6.97 | 6.64 | 6.95 |

| Residual Fuel Oil | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Fuels used in Electricity Generation | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.34 | 0.35 | 0.36 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 3.18 | 3.22 | 3.04 | 2.86 | 3.11 | 3.56 |

| Fuels used in Industry | 4.72 | 4.55 | 4.67 | 4.35 | 4.06 | 4.23 | 3.54 | 3.23 | 3.84 | 5.19 | 8.28 | 5.97 | 5.74 | 6.65 | 6.99 | 6.81 | 6.71 | 6.70 | 6.73 |

| Coal | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.59 | 1.59 | 1.59 | 1.59 | 1.59 | 1.59 | 1.59 | 1.59 | 2.25 | 2.68 | 3.51 | 3.38 | 3.17 | 3.42 |

| Peat | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.30 | 2.80 | 3.30 | 3.29 | 3.29 | 3.28 |

| Kerosene | 16.53 | 16.53 | 16.53 | 16.53 | 16.53 | 16.50 | 10.28 | 3.96 | 3.96 | 7.92 | 17.80 | 22.76 | 26.11 | 27.65 | 27.76 | 27.79 | 27.79 | 27.79 | 27.73 |

| Fuel Oil | 3.39 | 3.39 | 3.39 | 3.39 | 3.39 | 3.88 | 4.03 | 4.26 | 6.20 | 9.70 | 17.01 | 10.72 | 6.78 | 9.59 | 8.93 | 13.04 | 15.40 | 11.97 | 12.17 |

| LPG | 11.58 | 11.58 | 11.58 | 11.58 | 11.58 | 12.58 | 6.02 | 0.00 | 0.00 | 0.00 | 4.31 | 13.91 | 15.73 | 7.85 | 16.13 | 22.75 | 20.77 | 22.42 | 23.62 |

| Diesel/Gas Oil | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 19.43 | 19.22 | 19.30 | 19.52 | 23.26 | 35.65 | 35.46 | 40.14 | 41.60 | 44.00 | 43.76 | 43.68 | 43.65 | 43.67 |

| Petroleum Coke | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.06 | 2.45 | 2.78 | 2.89 | 3.05 | 3.21 |

| Natural Gas | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.40 | 0.35 | 0.34 | 0.31 | 0.29 | 0.27 |

| Fuels used in Services | 12.44 | 12.30 | 12.33 | 11.29 | 10.73 | 11.36 | 9.31 | 7.57 | 7.20 | 8.32 | 19.72 | 21.94 | 26.08 | 26.91 | 27.23 | 26.85 | 27.17 | 26.51 | 26.41 |

| Coal | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.79 | 1.59 | 1.59 | 1.59 | 1.59 | 1.59 | 1.59 | 1.59 | 4.47 | 12.47 | 17.61 | 9.49 | 8.93 | 11.84 |

| Peat | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Kerosene | 16.53 | 16.53 | 16.53 | 16.53 | 16.53 | 16.53 | 10.30 | 3.96 | 3.96 | 7.92 | 17.92 | 22.92 | 27.92 | 27.92 | 27.92 | 27.92 | 27.92 | 27.92 | 27.92 |

| LPG | 11.58 | 11.58 | 11.58 | 11.58 | 11.58 | 13.30 | 6.38 | 0.00 | 0.00 | 0.00 | 5.85 | 15.00 | 18.33 | 20.00 | 20.00 | 20.00 | 20.00 | 20.00 | 20.00 |

| Diesel/Gas Oil | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 25.10 | 35.10 | 40.10 | 45.10 | 45.11 | 45.11 | 45.11 | 45.11 | 45.12 | 45.14 |

| Natural Gas | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 10.00 | 15.00 | 20.00 | 20.07 | 20.07 | 20.06 | 20.06 | 20.06 | 20.05 |

| Marked Gas Oil used in Agriculture and Fishing | 18.81 | 18.80 | 19.13 | 18.30 | 17.82 | 18.33 | 18.51 | 18.55 | 19.07 | 21.30 | 38.56 | 38.30 | 38.15 | 37.33 | 37.18 | 36.90 | 37.02 | 37.08 | 39.44 |

| Household Heating Fuels | 8.74 | 9.17 | 9.42 | 9.63 | 9.59 | 9.85 | 7.58 | 5.55 | 5.69 | 7.33 | 14.09 | 18.79 | 21.50 | 21.18 | 22.39 | 23.71 | 24.52 | 24.10 | 24.58 |

| Coal | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 4.85 | 13.19 | 18.57 | 22.27 | 17.19 | 19.54 |

| Peat | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.97 | 5.04 | 6.85 | 7.25 | 5.91 | 7.53 |

| Kerosene | 16.53 | 16.53 | 16.53 | 16.53 | 16.53 | 16.53 | 10.30 | 3.96 | 3.96 | 7.92 | 17.92 | 22.92 | 27.92 | 27.92 | 27.92 | 27.92 | 27.92 | 27.92 | 27.92 |

| LPG | 11.58 | 11.58 | 11.58 | 11.58 | 11.58 | 13.30 | 6.38 | 0.00 | 0.00 | 0.00 | 10.00 | 15.00 | 18.33 | 20.00 | 20.00 | 20.00 | 20.00 | 20.00 | 20.00 |

| Diesel/Gas Oil | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 21.38 | 25.10 | 35.10 | 40.10 | 45.10 | 45.10 | 45.10 | 45.10 | 45.10 | 45.10 | 45.10 |

| Natural Gas | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 6.70 | 15.00 | 18.33 | 20.00 | 20.00 | 20.00 | 20.00 | 20.00 | 20.00 |

| Electricity Consumption | 0.00 | 0.00 | 0.00 | 0.00 | 5.04 | 6.69 | 2.95 | 0.00 | 0.00 | 0.15 | 3.43 | 12.19 | 8.45 | 13.75 | 21.88 | 28.19 | 27.29 | 35.54 | 39.99 |

| Table 2: Fossil Fuel Subsidies by Type, 2000-2018 | |||

| €m | |||

| Year | Direct Subsidies | Indirect Subsidies | Total Fossil Fuel Subsidies |

| 2000 | 79 | 1,340 | 1,420 |

| 2001 | 82 | 1,422 | 1,504 |

| 2002 | 101 | 1,494 | 1,595 |

| 2003 | 149 | 1,355 | 1,504 |

| 2004 | 188 | 1,570 | 1,758 |

| 2005 | 232 | 1,996 | 2,227 |

| 2006 | 225 | 2,099 | 2,325 |

| 2007 | 200 | 2,026 | 2,226 |

| 2008 | 225 | 2,171 | 2,395 |

| 2009 | 348 | 1,737 | 2,085 |

| 2010 | 357 | 1,785 | 2,142 |

| 2011 | 341 | 1,702 | 2,043 |

| 2012 | 389 | 1,614 | 2,003 |

| 2013 | 391 | 1,542 | 1,933 |

| 2014 | 456 | 1,611 | 2,066 |

| 2015 | 390 | 1,724 | 2,114 |

| 2016 | 352 | 1,737 | 2,089 |

| 2017 | 354 | 1,884 | 2,238 |

| 2018 | 300 | 2,124 | 2,424 |

| Table 3A: Direct Fossil Fuel Subsidies, 2010-2018 | |||||||||

| €m | |||||||||

| Direct Fossil Fuel Subsidies | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| Total | 356.8 | 340.7 | 389.1 | 390.7 | 455.7 | 390.3 | 351.9 | 354.3 | 299.6 |

| Fossil Fuel Production | |||||||||

| Petroleum Exploration & Production Promotion & Support | 1.3 | 1.3 | 1.3 | 0.5 | 1.6 | 2.0 | 2.4 | 2.1 | 1.2 |

| Science Foundation Ireland Fossil Fuel R&D Funding | – | – | – | – | – | 0.3 | 0.9 | 1.3 | 1.3 |

| Government Fossil Fuel R&D Funding | 0.1 | – | – | – | – | – | – | – | – |

| Fossil Fuel Consumption | |||||||||

| PSO Levy: Electricity Generation from Peat | 78.2 | 41.6 | 94.2 | 94.8 | 119.0 | 121.9 | 115.4 | 117.8 | 65.5 |

| PSO Levy: Security of Supply | 14.0 | 20.7 | 42.2 | 61.0 | 104.7 | 47.3 | 0.0 | 0.0 | 0.0 |

| Electricity Allowance | 144.7 | 146.5 | 141.7 | 126.8 | 118.2 | 111.4 | 110.3 | 110.2 | 103.2 |

| Gas Allowance | 20.0 | 20.7 | 20.6 | 16.3 | 21.8 | 18.8 | 19.2 | 20.6 | 19.3 |

| Fuel Allowance | 88.8 | 104.6 | 84.6 | 91.3 | 87.1 | 85.7 | 92.4 | 90.5 | 96.1 |

| Other Supplements (including Heating) | 5.4 | 5.1 | 4.5 | – | 3.2 | 3.0 | 2.7 | 2.3 | 3.1 |

| Smokeless Coal Allowance | 4.2 | – | – | – | – | – | – | – | – |

| Fuel Grant for Disabled Drivers/Passengers | – | – | – | – | – | – | 8.6 | 9.5 | 10.0 |

| – Scheme not in operation or no payments made | |||||||||

| Table 3B: Direct Fossil Fuel Subsidies, 2000-2009 | ||||||||||

| €m | ||||||||||

| Direct Fossil Fuel Subsidies | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 |

| Total | 79.2 | 81.5 | 100.7 | 149.1 | 187.9 | 231.8 | 225.0 | 199.9 | 224.8 | 348.2 |

| Fossil Fuel Production | ||||||||||

| Petroleum Exploration & Production Promotion & Support | 1.3 | 1.3 | 1.2 | 1.1 | 1.2 | 1.3 | 1.3 | 1.3 | 1.3 | 1.3 |

| Government Fossil Fuel R&D Funding | 0.2 | 0.3 | 0.1 | 0.4 | 0.3 | 0.6 | 0.4 | 0.4 | 0.4 | 0.1 |

| Fossil Fuel Consumption | ||||||||||

| PSO Levy: Electricity Generation from Peat | – | – | 0.0 | 38.9 | 58.4 | 62.7 | 65.1 | 0.0 | 0.0 | 84.5 |

| PSO Levy: Security of Supply | – | – | 0.0 | 0.0 | 0.0 | 20.0 | 0.0 | 0.0 | 0.0 | 18.2 |

| Electricity Allowance | 44.8 | 48.8 | 59.0 | 68.6 | 82.6 | 96.4 | 105.0 | 118.3 | 135.7 | 142.3 |

| Gas Allowance | 2.2 | 2.6 | 3.2 | 4.7 | 5.6 | 6.4 | 8.0 | 13.6 | 15.3 | 17.7 |

| Fuel Allowance | 26.6 | 24.5 | 32.2 | 34.8 | 33.9 | 33.0 | 34.0 | 54.7 | 60.4 | 77.4 |

| Other Supplements (including Heating) | 4.3 | 4.1 | 5.0 | 0.5 | 5.8 | 5.4 | 5.4 | 5.5 | 5.7 | – |

| Smokeless Coal Allowance | – | – | – | – | – | 6.0 | 5.9 | 6.0 | 6.0 | 6.6 |

| – Scheme not in operation or no payments made | ||||||||||

| Table 4A: Indirect Fossil Fuel Subsidies (Tax Expenditures), 2010-2018 | ||||||||||

| €m | ||||||||||

| Indirect Fossil Fuel Subsidies | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

| Total | 1,785.5 | 1,702.2 | 1,613.8 | 1,541.9 | 1,610.8 | 1,723.8 | 1,736.7 | 1,884.1 | 2,123.9 | |

| Fossil Fuel Production | ||||||||||

| Revenue Foregone: Royalties on Gas and Oil Production | .. | .. | .. | .. | .. | 0.0 | 50.2 | 71.0 | 90.6 | |

| Road Transport Fuels | ||||||||||

| Revenue Foregone: Excise Duty on Autodiesel | 240.6 | 283.3 | 276.9 | 290.9 | 309.4 | 337.5 | 362.0 | 388.2 | 390.1 | |

| Autodiesel VAT Refund | 273.9 | 259.8 | 296.8 | 312.7 | 307.0 | 299.3 | 241.7 | 236.7 | 284.6 | |

| Diesel Rebate Scheme | – | – | – | 0.7 | 21.1 | 13.1 | 1.3 | 0.8 | 3.4 | |

| Fuel Excise Repayment for Disabled Drivers/Passengers | 5.1 | 7.4 | 7.8 | 7.7 | 7.6 | 5.3 | – | – | – | |

| Revenue Foregone: Excise Duty on Auto LPG | 0.2 | 0.2 | 0.4 | 1.0 | 1.8 | 2.1 | 2.1 | 1.9 | 1.5 | |

| Other Transport Fuels & Fuels used in Industry | ||||||||||

| Jet Kerosene Excise Exemption | 419.5 | 386.3 | 332.6 | 383.7 | 425.2 | 480.9 | 494.0 | 580.4 | 626.5 | |

| Aviation Gasoline Excise Repayment | .. | .. | .. | .. | .. | .. | .. | .. | 0.1 | |

| Free ETS Emission Permits: Aircraft Operators | – | – | 50.6 | 23.7 | 31.9 | 40.9 | 28.4 | 31.0 | 85.2 | |

| Fuel Excise Repayment for Commercial Sea Navigation | 5.0 | 5.7 | 6.6 | 6.8 | 8.5 | 8.4 | 10.1 | 8.9 | 0.0 | |

| Marine Diesel Scheme (VAT) | 0.1 | 0.1 | 0.1 | 0.2 | 0.1 | 0.1 | 0.1 | 0.1 | 0.0 | |

| Revenue Foregone: Excise Duty on Marked Gas Oil | 253.1 | 251.3 | 256.2 | 259.7 | 249.0 | 253.7 | 266.0 | 262.9 | 273.2 | |

| Free ETS Emission Permits: Stationary Installations | 302.1 | 271.6 | 160.0 | 23.5 | 28.4 | 40.9 | 27.7 | 29.9 | 78.7 | |

| Fuel Oil Excise Exemption for Manufacture of Alumina | 3.3 | 2.2 | 1.3 | 1.3 | 0.6 | 0.0 | 0.0 | 0.0 | – | |

| Fuel Excise Repayment for Horticulture | 0.1 | 0.7 | 0.1 | 0.1 | 0.1 | 0.1 | 0.0 | 0.1 | 0.0 | |

| Revenue Foregone: Excise Duty on Fuel Oil | 61.5 | 42.6 | 38.3 | 34.8 | 29.8 | 27.7 | 27.6 | 28.8 | 24.5 | |

| Carbon Tax Repayments | – | .. | .. | .. | .. | .. | .. | 0.9 | 5.7 | |

| Fuels used for Heating | ||||||||||

| Revenue Foregone: Excise Duty on Kerosene | 143.9 | 117.4 | 93.8 | 90.5 | 85.6 | 101.5 | 105.3 | 109.0 | 115.2 | |

| Revenue Foregone: Excise Duty on Non-auto LPG | 63.5 | 60.6 | 80.2 | 92.6 | 93.2 | 100.5 | 108.6 | 122.4 | 133.5 | |

| Electricity Consumption | ||||||||||

| Electricity Excise Exemption: Domestic Use | 7.2 | 6.8 | 6.5 | 6.3 | 5.9 | 5.9 | 5.8 | 5.6 | 5.5 | |

| Revenue Foregone: Excise Duty on Business Electricity Use | 6.3 | 6.0 | 5.7 | 5.7 | 5.6 | 5.7 | 5.8 | 5.6 | 5.6 | |

| .. Not available | ||||||||||

| – Scheme not in operation or no payments made | ||||||||||

| Table 4B: Indirect Fossil Fuel Subsidies (Tax Expenditures), 2000-2009 | ||||||||||

| €m | ||||||||||

| Indirect Fossil Fuel Subsidies | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 |

| Total | 1,340.4 | 1,422.2 | 1,494.5 | 1,354.8 | 1,569.9 | 1,995.7 | 2,099.5 | 2,025.9 | 2,170.6 | 1,737.2 |

| Fossil Fuel Production | ||||||||||

| Revenue Foregone: Royalties on Gas and Oil Production | – | – | – | 8.0 | 4.5 | .. | .. | .. | .. | .. |

| Road Transport Fuels | ||||||||||

| Revenue Foregone: Excise Duty on Autodiesel | 96.9 | 213.8 | 225.0 | 171.6 | 182.4 | 193.7 | 211.7 | 225.8 | 220.9 | 270.3 |

| Autodiesel VAT Refund | 138.4 | 117.7 | 144.5 | 165.2 | 191.5 | 230.9 | 237.7 | 252.4 | 369.8 | 255.9 |

| Fuel Excise Repayment for Disabled Drivers/Passengers | 2.6 | 2.6 | 3.2 | 3.6 | 4.2 | 4.8 | 5.2 | 5.5 | 6.0 | 6.9 |

| Revenue Foregone: Excise Duty on Auto LPG | 1.1 | 0.8 | 0.8 | 0.7 | 0.7 | 0.7 | 0.6 | 0.4 | 0.3 | 0.2 |

| Other Transport Fuels & Fuels used in Industry | ||||||||||

| Jet Kerosene Excise Exemption | 242.4 | 223.2 | 287.4 | 304.0 | 324.5 | 374.3 | 431.5 | 456.0 | 423.7 | 372.5 |

| Fuel Excise Repayment for Commercial Sea Navigation | 0.8 | 1.0 | 1.6 | 2.1 | 3.0 | 2.7 | 4.4 | 3.5 | 3.6 | 3.5 |

| Marine Diesel Scheme (VAT) | – | – | – | – | 0.0 | 0.0 | 0.0 | 0.2 | 0.2 | 0.1 |

| Revenue Foregone: Excise Duty on Marked Gas Oil | 223.4 | 212.2 | 235.3 | 248.1 | 292.6 | 293.8 | 310.4 | 293.6 | 271.9 | 274.7 |

| Free ETS Emission Permits: Stationary Installations | – | – | – | – | – | 335.1 | 335.1 | 335.1 | 480.6 | 276.0 |

| Fuel Oil Excise Exemption for Manufacture of Alumina | 4.9 | 4.6 | 4.4 | 4.8 | 4.4 | 5.1 | 3.8 | 3.3 | 3.1 | 2.0 |

| Fuel Excise Repayment for Horticulture | 0.3 | 0.2 | 0.4 | 0.3 | 0.3 | 0.3 | 0.2 | 0.2 | 0.2 | 0.2 |

| Revenue Foregone: Excise Duty on Fuel Oil | 509.0 | 523.3 | 454.8 | 300.2 | 399.6 | 390.3 | 369.3 | 237.5 | 176.2 | 67.6 |

| Fuels used for Heating | ||||||||||

| Revenue Foregone: Excise Duty on Kerosene | 47.5 | 53.6 | 60.1 | 66.1 | 72.2 | 74.5 | 95.6 | 113.6 | 121.5 | 137.5 |

| Revenue Foregone: Excise Duty on Non-auto LPG | 61.2 | 56.8 | 64.4 | 67.1 | 76.7 | 75.7 | 79.5 | 84.6 | 78.1 | 56.3 |

| Electricity Consumption | ||||||||||

| Electricity Excise Exemption: Domestic Use | 6.1 | 6.4 | 6.3 | 6.6 | 6.9 | 7.0 | 7.4 | 7.3 | 7.6 | 7.0 |

| Revenue Foregone: Excise Duty on Business Electricity Use | 5.9 | 6.0 | 6.3 | 6.5 | 6.3 | 6.7 | 7.1 | 6.9 | 6.9 | 6.4 |

| .. Not available | ||||||||||

| – Scheme not in operation or no payments made | ||||||||||

In this release we calculated the average effective carbon rates of different fossil fuels in different sectors of the Irish economy. These effective carbon rates can be compared to a reference carbon price. The difference between the revenue that would be accrued at the reference price and the actual revenue accrued at the effective carbon rate is one possible approach to measuring fossil fuel subsidies.

The OECD maintains a database of national energy taxes called the Taxing Energy Use database and uses it to report effective carbon rates for different sectors and fuels in OECD countries. We used similar concepts to the OECD but developed our own methodology for this release.

The average effective carbon rate for a fuel is defined as total energy taxes paid divided by the total amount of carbon dioxide emitted through combustion of the fuel. The energy taxes included were Excise Duty, Carbon Tax, Electricity Tax, the Public Service Obligation (PSO) Levy, the National Oil Reserves Agency (NORA) Levy and emission permit purchases under the EU Emissions Trading Scheme. These taxes are included as energy taxes in the CSO’s Environment Taxes release. VAT was not included in the calculation of the effective carbon rate as it applies to non-energy products as well, although it should be noted that a reduced rate of VAT applies to energy products.

The average effective carbon rate was calculated using net receipts and Excise volumes published by Revenue wherever possible. When net receipts or Excise volumes for a specific fuel or sector were not available, information on energy tax rates and reliefs were used in conjunction with energy use statistics from the SEAI Energy Balance to estimate receipts. Emissions were estimated from Excise volumes or Energy Balance statistics by applying emission factors published by the SEAI to fuel consumption.

The Excise Duty rates on mineral oils published by Revenue include a carbon component, which is also referred to as the Carbon Tax. The Carbon Tax rate is directly related to the amount of carbon dioxide emitted through combustion of the fuel while the non-carbon component of the Excise Duty rate depends on whether the fuel is used for transport, industry or heating. There is a separate Solid Fuel Carbon Tax on coal and peat and a Natural Gas Carbon Tax. There are many rate reductions and exemptions on Excise Duty and the Carbon Tax, such as the exemptions for fuel used in international aviation, maritime transport and electricity generation.

Electricity Tax is paid by business and non-business consumers. There is no tax on domestic use of electricity. All electricity consumers pay the PSO Levy, which is used to subsidise electricity generation.

The NORA Levy is charged at a rate of 2 cents per litre on oil products such as petrol, autodiesel and kerosene. The NORA Levy is used to fund the acquisition and storage of strategic oil stocks. It does not apply on fuel used for international aviation or maritime transport.

The EU Emissions Trading Scheme commenced in 2005. An emission permit allows the holder to emit one tonne of carbon dioxide. Major emitters of greenhouse gases were provided with free allowances of emission permits. They surrender a quantity of permits equal to their verified carbon dioxide emissions each year. If the free allowances do not cover their emissions they must purchase further permits at auction.

We calculated the average effective carbon rate for petrol, autodiesel and liquefied petroleum gasoline (auto LPG) using net receipts and Excise volumes published by Revenue. The taxes that applied to road transport fuels were Excise Duty, Carbon Tax and the NORA Levy. Petrol had the highest Excise Duty rate while the Carbon Tax and the NORA Levy applied equally to the three fuels.

We included diesel, charged at the rate of marked gas oil, and electricity under rail transport fuels. Excise Duty, Carbon Tax and the NORA Levy were charged on diesel, while Electricity Tax and the PSO Levy were charged on electricity. Electricity emissions were calculated using the CSO Business Energy Use survey data on energy use and SEAI electricity emission factors. Electricity Tax applied at the non-business rate of €0.50 per MWh while the PSO Levy payments were estimated using data obtained directly from Iarnród Éireann.

Aviation gasoline and jet kerosene are the main aviation fuels. Aviation gasoline for private use is subject to the same Excise Duty rate as petrol. However a partial Excise repayment is available on aviation gasoline for commercial use. Aviation gasoline volumes and partial Excise repayments were obtained from Revenue Excise volumes and by direct request to Revenue respectively. Net receipts were not available and were therefore estimated using the Excise Duty and Carbon Tax rates and reliefs.

Jet kerosene for commercial domestic and international use is exempt from Excise Duty, Carbon Tax and the NORA Levy. The exemption for international use is included in the EU Energy Taxation Directive, which permits taxation on jet kerosene used for domestic flights and for international flights between member states with bilateral agreements to impose taxes. Jet kerosene consumption was obtained from the SEAI Energy Balance. No tax applies to international consumption. We applied the Excise Duty and Carbon Tax rate on heavy oil for air navigation to a small proportion of domestic use of jet kerosene to estimate potential tax receipts.

Marine fuel for commercial use is exempt from Excise Duty, Carbon Tax and the NORA Levy.

Fuel use for private pleasure navigation is subject to Excise Duty and Carbon Tax at the same rate as autodiesel. We applied this rate to a proportion of domestic use of marine diesel to obtain an estimate of tax receipts from fuel use in privately owned boats.

Fuels used for electricity generation (excluding in combined heat and power (CHP) plants that have not been certified as high efficiency CHP) are exempt from Excise Duty, Carbon Tax and the NORA Levy. The electricity generation sector instead comes under the Emissions Trading Scheme (ETS). From 2005-2012, power plants were provided with free allowances which covered a large majority of their emissions, or even exceeded them. Since 2013 the electricity generation sector has received no further free allocation of emission permits. Taking into account the free allocation, the average effective carbon rate was much lower than the Carbon Tax rate that normally applied to the fuels used for electricity generation. The marginal rate, i.e. the price paid at auction for a permit to emit a single tonne of carbon dioxide, has also mostly been lower than the Carbon Tax rate since it was introduced.

We used energy data from the SEAI Energy Balance on coal, peat, fuel oil, diesel, natural gas and LPG to estimate emissions from the electricity generation sector. We used figures from the CSO’s Environment Taxes release on total national purchases and use of emission permits, or carbon credits, to estimate multi-annual purchases of ETS permits by the electricity generation sector. The average effective carbon rate was calculated as purchases of permits over total emissions.

Emissions included under the ETS are largely exempt from Excise Duty and Carbon Tax. Receipts from Industry sector purchases of ETS emission permits were estimated using data on carbon credits from the CSO’s Environment Taxes release. Tax receipts from non-ETS Industry sector emissions were estimated using energy use data from the SEAI Energy Balance along with information on tax rates and reliefs. We included coal, peat, kerosene, fuel oil, LPG, MGO, petroleum coke and natural gas in our calculation of an average effective carbon rate for fuel use in the Industry sector.

Receipts from Services sector purchases of ETS emission permits were estimated using data on carbon credits from the CSO’s Environment Taxes release. Tax receipts from non-ETS Services sector emissions were estimated using energy use data from the SEAI Energy Balance along with information on tax rates and reliefs. We included coal, peat, kerosene, LPG, MGO and natural gas in our calculation of an average effective carbon rate for fuel use in the Services sector.

We calculated the average effective carbon rate for marked gas oil (MGO) used in Agriculture and Fishing using energy data from the SEAI Energy Balance and information on the rates of Excise Duty, Carbon Tax and the NORA Levy that applied to MGO. MGO used for commercial sea-fishing is exempt from all three taxes.

The fuels used for household heating were coal, peat, kerosene, LPG, marked gas oil (MGO) and natural gas. A low, often zero, rate of Excise Duty applies to fuels used for heating. All are subject to Carbon Tax and the NORA Levy is also applied on kerosene and MGO. Energy use data were obtained from the SEAI Energy Balance and information on tax rates was used to calculate the average effective carbon rate.

We used electricity consumption data from the SEAI Energy Balance and SEAI electricity emission factors to calculate emissions from electricity consumption by all sectors. Net receipts of Electricity Tax were published by Revenue, and PSO Levy receipts were published in the CSO’s Environment Taxes release.

The UN System of Environmental-Economic Accounting (SEEA) is a statistical system that brings together economic and environmental information into a common framework to measure the condition of the environment, the contribution of the environment to the economy, and the impact of the economy on the environment. The SEEA contains an internationally agreed set of standard concepts, definitions, classifications, accounting rules and tables to produce internationally comparable statistics.

Eurostat has developed a series of legal and voluntary environmental accounts modules based on the SEEA. The CSO has published statistical releases on the Eurostat Environmental Taxes and Environmental Subsidies and Similar Transfers modules. This new release complements those two releases as it enables users to compare the amount raised through energy taxes with the amount spent on fossil fuel subsidies and further with the amount spent on environmental subsidies aimed at protecting the climate and the air, reducing fossil fuel consumption and increasing the share of renewables.

This new CSO release provides data for SDG goal 12.

Target 12.c Rationalise inefficient fossil-fuel subsidies that encourage wasteful consumption by removing market distortions, in accordance with national circumstances, including by restructuring taxation and phasing out those harmful subsidies, where they exist, to reflect their environmental impacts, taking fully into account the specific needs and conditions of developing countries and minimising the possible adverse impacts on their development in a manner that protects the poor and the affected communities.

Indicator 12.c.1 Amount of fossil-fuel subsidies per unit of GDP (production and consumption)

The OECD defines a subsidy as the result of a government action that confers an advantage on consumers or producers in order to supplement their income or lower their costs.

This definition is broader than the European System of Accounts definition. Although they do not appear in government budgets or accounts, the OECD definition includes tax expenditures as they constitute a loss of revenue by the government in order to support producer or consumer economic activity.

The CSO included schemes in this release if they met the following two criteria:

The CSO has not included any Environmental Subsidies and Similar Transfers (ESST) in this release nor any subsidies included here in the ESST release.

Support measures established for social policy reasons, such as fuel allowances, have been included in this release if they met the two criteria above.

For the purposes of this release, a support is considered a subsidy if it is one of the following types of transaction or assistance:

|

Type of Transfer |

ESA 2010 Definition |

|

Subsidies (D.3) |

Current unrequited payments which general government or the institutions of the European Union make to resident producers. |

|

Social transfers in kind (D.63) |

Goods and services provided for free or at prices that are not economically significant to individual households by government units and non-profit institutions. |

|

Other current transfers (D.7) |

Transfers between resident institutional units, or between resident and non-resident units, other than current taxes on income, wealth, etc., social contributions and benefits, and social benefits in kind. |

|

Investment grants (D.92) |

Capital transfers in cash or in kind made by governments or by the rest of the world to other institutional units to finance all or part of the costs of their acquiring fixed assets. |

|

Other capital transfers (D.99) |

Transfers other than investment grants and capital taxes which do not themselves redistribute income but redistribute saving or wealth among the different sectors or subsectors of the economy or the rest of the world. |

Fossil fuel activities include exploration, extraction, manufacturing, refining and distribution of fossil fuels on the production side, as well as research and development supporting any of the above. Fossil fuel consumption by all sectors of the economy is also included as a fossil fuel activity.

In this release, a fossil fuel subsidy is any subsidy that directly incentivises or supports an increase in these activities. Many transport subsidies indirectly cause an increase in fossil fuel consumption. Transport subsidies are not included as fossil fuel subsidies but a list of transport subsidies is included in the Background Notes for information.

We divided supports into direct supports such as investment grants, and indirect supports such as tax expenditures. Data on direct supports were mainly obtained from government appropriation accounts, the annual accounts of government departments and agencies, and through requests to the relevant government department or organisation. An example of a direct subsidy is the PSO Levy support to electricity generation from peat.

Tax expenditures are defined relative to a system of benchmark taxes. Benchmark tax rates are the standard, conventional rates applied to economic transactions and activities in the economy. Tax expenditures are reductions in potential revenue due to deviations from these standard rates. These lower rates are intended to incentivise behaviour that meets particular policy objectives. Data on tax expenditures were mainly obtained from Revenue, or estimated using information from Revenue. An example of a tax expenditure is the reduced excise duty on autodiesel compared with petrol.

The OECD has outlined three approaches to measuring tax expenditures:

The CSO uses the revenue foregone approach to calculating tax expenditures in this release. A table of benchmark taxes used for these calculations is shown below. A number of tax expenditures are due to reduced Excise Duty rates on certain fuels or on fuels used by certain sectors of the economy. A table of Excise Duty rates is also provided below.

The table shows the benchmark taxes used in this release for calculations of tax expenditures and the 2018 benchmark tax rates. The specific benchmark rates used in the release for 2000-2017 are outlined in the Excise Duty rates table below.

| Type of Tax | Specific Tax from Irish Regime | Unit | Tax Rate in 2018 |

|---|---|---|---|

| Excise Duty on Hydrocarbon Oils used in Transport/Industry (inclusive of Carbon Tax) | Excise Duty on Petrol (inclusive of Carbon Tax) | € per 1,000 litres | 587.71 |

| Excise Duty on Hydrocarbon Oils used for Heating (inclusive of Carbon Tax) | Energy Tax on Marked Gas Oil (inclusive of Carbon Tax) | € per 1,000 litres | 102.28 |

| Excise Duty on Electricity | Electricity Tax for non-Business Use | € per Megawatt-hour | 1.00 |

| VAT on Energy Products | Standard VAT Rate | % of price excluding VAT |

23 |

The table shows the 2018 Excise Duty and Carbon Tax rates used in this release for calculations of tax expenditures, and briefly outlines some of the Excise and Carbon rates used for 2000-2017. The table does not show all Excise and Carbon Tax rates from 2000-2017.

| Energy Product | € per 1,000 litres, 2018 | € per 1,000 litres, 2000-2017 |

| Unleaded Petrol | 587.71 | Excise Duty on petrol was €373.94 per 1,000 litres in 2000, €384.54 in 2001, €401.36 from 2002-2003, €442.68 from 2004 to 2008, €508.79 in 2009, €543.17 in 2010, €576.22 in 2011, and was unchanged between 2012 and 2018 |

| of which carbon tax | 45.87 | Carbon Tax on petrol was introduced in December 2009 |

| Autodiesel | 479.02 | Excise Duty on autodiesel was €325.30 per 1,000 litres in 2000, €249.10 in 2001, €301.94 in 2002, €326.73 in 2003, €368.05 from 2004 to 2008, €409.20 in 2009, €449.18 in 2010, €465.70 in 2011 and was unchanged from 2012 to 2018 |

| of which carbon tax | 53.30 | Carbon Tax on autodiesel was introduced in December 2009 |

| Liquefied Petroleum Gas (LPG) | 96.45 | Excise Duty on LPG was €53.01 per 1,000 litres from 2000 to 2004, €63.59 from 2005 to 2009 and was unchanged from 2012 to 2018 |

| of which carbon tax | 32.86 |

Carbon Tax on LPG was introduced in May 2010 |

| Heavy Oil used in Air Navigation (Jet Kerosene) | 479.02 | See Autodiesel entry for historical rates. These rates apply to jet kerosene for non-commercial use only |

| of which carbon tax | 53.30 | Carbon Tax on jet kerosene for non-commercical use was introduced in May 2010 |

| Aviation Gasoline | 587.71 | See Petrol entry for historical rates |

| of which carbon tax | 45.87 | Carbon Tax on aviation gasoline was introduced in May 2010 |

| Marked Gas Oil | 102.28 | Excise Duty on marked gas oil was €47.36 per thousand litres from 2000 to 2009 and was unchanged from 2010 to 2018 |

| of which carbon tax | 54.92 | Carbon Tax on MGO was introduced in May 2010 |

| Kerosene | 50.73 | Excise Duty on kerosene was €31.74 per 1,000 litres from 2000 to 2005, €16.00 in 2006 and €0.00 from 2007 to 2009. The non-carbon component remained at €0.00 since then and the total rate is equal to the carbon component. |

| of which carbon tax | 50.73 | Carbon Tax on kerosene was introduced in May 2010 |

| Fuel Oil | 76.53 | Excise Duty on fuel oil was €13.45 per 1,000 litres in 2000, €14.78 from 2005 to 2009, and was unchanged from 2013 to 2018 |

| of which carbon tax | 61.75 | Carbon Tax on fuel oil was introduced in May 2010 |

| Liquefied Petroleum Gas (LPG) | 32.86 | Excise Duty on non-auto LPG was €18.16 per thousand litres in 2000 and €0.00 from 2007 to 2009. The non-carbon component remained at €0.00 since then and the total rate is equal to the carbon component. |

| of which carbon tax | 32.86 | Carbon Tax on LPG was introduced in May 2010 |

| Electricity Tax | € per Megawatt-hour | |

| Non-business Use | 1.00 | Excise Duty on electricity has been levied at the rate of €1.00 per Megawatt-hour for non-business use since its introduction in 2009 |

| Business Use | 0.50 | Excise Duty on electricity has been levied at the rate of €0.50 per Megawatt-hour for business use since its introduction in 2009 |

| Domestic Use | 0.00 | Domestic use of electricity has always been exempt from Excise Duty |

The figures are subject to revision on an ongoing basis. A full list of fossil fuel subsidies we have identified is provided in the next section of the Background Notes. Data are not currently available for all of these subsidies but estimates may be made where possible in future releases.

The CSO previously published a research paper on Fossil Fuel and Similar Subsidies, 2012-2016. In this release we have revised our figures or calculations for certain subsidies. Subsidies relating to electricity have been adjusted to account for the proportion of electricity generated from renewable sources in Ireland. The Heating Supplement has been adjusted to take account of the fact that it is only partly a payment in support of heating needs. The Fuel Allowance has been adjusted to take account of the possibility that it may be partly used for non-fossil fuels such as wood, and because the full amount of the allowance may not be used to purchase fuel. Separate benchmark tax rates for transport/industry and heating have been applied resulting in a reduction in the revenue foregone attributed to the Excise rates on marked gas oil, kerosene and fuel oil. A number of subsidies have been identified that were not included in the research paper and data have been obtained or estimated for some of these subsidies.

| Direct Fossil Fuel Subsidies | In operation in 2018? | Data Availability? |

| Fossil Fuel Production | ||

| Petroleum Exploration and Production Promotion and Support (PEPPS) Programme | Y | Y |

| Government Fossil Fuel R&D Funding | Y | Y |

| SFI Funding to Fossil Fuel Research | Y | Y |

| Fossil Fuel Consumption | ||

| PSO Levy: Electricity Generation from Peat | Y | Y |

| PSO Levy: Security of Electricity Supply | Y | Y |

| Electricity Allowance | Y | Y |

| Gas Allowance | Y | Y |

| Fuel Allowance | Y | Y |

| Other Supplements (including Heating) | Y | Y |

| Smokeless Coal Allowance | N | Y |

| Fuel Grant for Disabled Drivers and Passengers | Y | Y |

| Indirect Fossil Fuel Subsidies | Payment | In operation in 2018? | Data Availability? |

| Fossil Fuel Production | |||

| Zero Royalties on Gas and Oil Production | Royalty | Y | Y |

| Expensing of Exploration and Development Costs | Corporation Tax | Y | N |

| Stamp Duty Relief on Licences and leases granted under Petroleum and Other Mineral Development Act, 1960, etc. | Stamp Duty | Y | N |

| Road Transport Fuels | |||

| Diesel Rebate Scheme | Excise | Y | Y |

| Fuel Excise Repayment for Disabled Drivers and Passengers | Excise | N | Y |

| Revenue Foregone: Autodiesel | Excise | Y | Y |

| Revenue Foregone: Auto LPG | Excise | Y | Y |

| Revenue Foregone: Scheduled Passenger Road Transport Services | Excise | N | N |

| Autodiesel VAT Refund | VAT | Y | Y |

| Air, Water, Rail Transport Fuels | |||

| Fuel Excise Repayment for Commercial Sea Navigation | Excise | Y | Y |

| Jet Kerosene Excise Exemption | Excise | Y | Y |

| Free Allocation of Emissions Allowances to Airline Operators within EU-ETS | Cost of Allowances | Y | Y |

| Revenue Foregone: Marked Gas Oil for Rail Transport | Excise | Y | Y |

| Partial Excise Repayment on Aviation Gasoline used for Commercial Purposes | Excise | Y | Y |

| Marine Diesel Scheme | VAT | Y | Y |

| Zero VAT on Jet Kerosene for International Flights | VAT | Y | N |

| Fuels used in Industry | |||

| Fuel Oil Excise Exemption for Manufacture of Alumina | Excise | N | Y |

| Fuel Excise Repayment for Horticulture | Excise | Y | Y |

| Revenue Foregone: Marked Gas Oil for Agriculture, Fishing, Industry | Excise | Y | Y |

| Natural Gas Carbon Tax Exemption for Certain Industrial Uses | Carbon Tax | Y | N |

| Solid Fuel Carbon Tax Exemption for Certain Industrial Uses | Carbon Tax | Y | N |

| Relief for Increase in Carbon Tax on Farm Diesel | Carbon Tax | Y | N |

| Free Allocation of Emissions Allowances to Companies within EU-ETS | Cost of Allowances | Y | Y |

| Revenue Foregone: Fuel Oil | Excise | Y | Y |

| Heating Fuels | |||

| Revenue Foregone: Kerosene | Excise | Y | Y |

| Revenue Foregone: Non-auto LPG | Excise | Y | Y |

| Zero Excise on Coal | Excise | Y | N |

| Zero Excise on Peat | Excise | Y | N |

| Zero Excise on Natural Gas | Excise | Y | N |

| Solid Fuel Carbon Tax Exemption under Diplomatic Arrangements | Carbon Tax | Y | N |

| Reduced VAT rate on Energy Products | VAT | Y | N |

| Electricity | |||

| Electricity Excise Exemption for Domestic Use | Excise | Y | Y |

| Revenue Foregone: Business Electricity Use | Excise | Y | Y |

| Relief from Taxation on Electricity used for Certain Industrial Purposes/Generated in Certain Circumstances | Excise | Y | N |

Petroleum Exploration and Production Promotion and Support (PEPPS) Programme

The Petroleum Infrastructure Programme (PIP) was set up by the Petroleum Affairs Division (PAD) of the Department of Communications, Marine and Natural Resources in 1997. It consisted of three sub-programmes: the Offshore Support Group, the Rockall Studies Group, and the Porcupine Studies Group.

It was replaced by the Petroleum Exploration and Production Promotion and Support (PEPPS) in 2003. PEPPS consists of two sub-programmes, the Expanded Offshore Support Group and the Irish Shelf Petroleum Study Group (ISPSG).

The overall aims of PIP/PEPPS are to promote hydrocarbon exploration and development activities by strengthening local support structures and funding research.

PIP/PEPPS are funded by oil and gas companies with Irish offshore exploration licences.

Some of the funding has been used for environment-related research, for example the ObSERVE programme, which was an aerial and acoustic marine wildlife survey carried out from 2015-2018. These amounts have been excluded from the funding reported here.

Government R&D Petroleum and Coal

These figures are submitted by the SEAI to the International Energy Agency (IEA) annually. The IEA maintains a database of fossil fuel research funding. In recent years the research, although reported as relating to fossil fuels, appears to be largely environmentally motivated, and has not therefore been included here.

Science Foundation Ireland (SFI) Funding of Irish Centre for Research in Applied Geosciences (iCRAG)

ICRAG carries out research under a number of pillars, including Energy Security. This SFI-funded research is aimed at "finding and producing hydrocarbons from offshore sedimentary basins". In addition the purpose is "to strengthen Ireland’s position as an international leader in key hydrocarbon research themes, and to advise government in optimising exploration and development strategies by provision of independent scientific information and exploration models." The centre partners with a number of petroleum companies as well as other industry partners, and offers membership packages with benefits such as "substantial risk mitigation for Irish exploration activity" and "tax relief options under Ireland’s R&D Tax Credit Regime". ICRAG also carries out research into environmental protection areas such as marine geoscience and groundwater protection. This funding will be included in the CSO Environmental Subsidies release.

Zero Royalties on Gas and Oil Production

The tax regime in Ireland was overhauled between 1987 and 1992 with the policy aim of incentivising fossil fuel activities by petroleum companies. The fiscal terms that apply to production from a Petroleum Lease are determined by the date of the award of the initial authorisation. In certain circumstances it is possible for production from leases obtained between 1987 and 2014 to result in no tax or royalty payments, e.g. if capital costs are used to write off the corporation tax that would otherwise owe on profits. Before 1987 and after 2014 a minimum payment was due in all circumstances, charged on gross revenue from the field. We have used a simple approach to obtain an estimate of the fossil fuel subsidy to producers in Ireland by calculating it as a royalty of 12.5% that would owe on the gross revenue from a producing field.

Expensing of Exportation and Development Costs

Capital expenditure on exploration, development and production extending back 25 years, including on fields other than the field in production, can be written off at a rate of 100% against profits from the field. It should be noted that all companies are allowed to write off their expenses against tax on their profits but also that the these “tax losses” can be carried forward indefinitely by oil and gas companies. There are no data available on this subsidy.

Stamp Duty Relief on Licences and Leases granted under Petroleum and Other Mineral Development Act, 1960, etc.

In 2013 there were 11 claims for this relief at a cost of €10,000, according to the Department of Finance report on Tax Expenditures from October 2015. Since then the number of claims has been below ten and the cost has not been estimated, or data are not available. There are no data available for years previous to 2013.

PSO Levy: Electricity Generation from Peat and Security of Electricity Supply

The PSO Levy is charged to electricity consumers in Ireland and is used to subsidise electricity generation from peat and from renewable sources, as well as generation from fossil fuels to ensure security of supply. We have included the portions that go towards electricity generation from peat and security of supply as fossil fuel subsidies while the portion that supports electricity generation from renewable sources is included as an environmental subsidy in our Environmental Subsidies and Similar Transfers release.

The Commission for the Regulation of Utilities (CRU) publishes an annual decision paper on the amount of the subsidy from October 1st in a given year until September 30th the following year. We have assigned the figure published by the CRU to the calendar year in which the majority of the subsidy year lies.

A summary analysis of the type of subsidy, the beneficiary, the reason for including it in this release, and the data source is provided below:

Fuel Grant for Disabled Drivers and Disabled Passengers Scheme

The Disabled Drivers and Disabled Passengers Scheme provides a range of tax reliefs linked to the purchase and use of specially constructed or adapted vehicles by drivers and passengers with a disability. A person who qualifies for tax relief under the Disabled Drivers and Disabled Passengers Scheme will also qualify for the fuel grant.

Diesel Rebate Scheme

The Diesel Rebate Scheme came into effect on 1 July 2013. To qualify for inclusion in this scheme, road transport operators must hold an appropriate road transport licence. Road haulage operators must hold either a national or international road haulage operator's licence, while passenger transport operators must hold either a national road passenger transport operator’s licence or international road passenger transport operator’s licence.

Fuel Excise Repayment for Disabled Drivers and Disabled Passengers

This scheme was a precursor to the Fuel Grant. It was a repayment of excise duty on transport fuels for disabled drivers and passengers.

Revenue Foregone: Autodiesel

Excise duty (including carbon tax) on autodiesel was €479.02 per 1,000 litres in 2018. Excise duty (including carbon tax) on petrol was €587.71 per 1,000 litres. The revenue foregone by the State due to the reduced tax rate on autodiesel compared to a benchmark or reference rate of the excise duty on petrol is calculated as the difference in the rates multiplied by the volume of autodiesel purchased.

Revenue Foregone: Auto LPG

Excise duty (including carbon tax) on auto LPG was €96.45 per 1,000 litres in 2018. Excise duty (including carbon tax) on petrol was €587.71 per 1,000 litres. The revenue foregone by the State due to the reduced tax rate on auto LPG compared to a benchmark or reference rate of the excise duty on petrol is calculated as the difference in the rates multiplied by the volume of auto LPG purchased.

Revenue Foregone: Scheduled Passenger Road Transport Services

This reduced excise rate of €22.72 per 1,000 litres for road transport operators was in place until 2008. Road passenger services can now avail of a rebate on autodiesel under the Diesel Rebate Scheme (see above).

Autodiesel VAT Refund

Businesses in Ireland can apply for a refund of VAT paid on autodiesel used for business purposes. The figures are estimated by the CSO using business expenditure on autodiesel from 2009-2017 from the CSO's Business Energy Use survey. Estimates for other years use the SEAI Energy Balances and pricing data from the CSO. It is important to note that the estimates will exceed the actual amount of VAT refunded to businesses as an assumption is made that all possible amounts are claimed in refunds.

Fuel Excise Repayment for Commercial Sea Navigation

This scheme follows from a European Council Directive which sets a low minimum rate of taxation on energy products supplied for use as fuel for the purposes of navigation within Community waters (including fishing).

Jet Kerosene Excise Exemption

This is a tax exemption for jet kerosene used for commercial aviation. The figures are estimated using the volume of jet kerosene purchased in Ireland as published by the SEAI (Energy Balances). The reference excise charge was taken to be the rate on heavy oil used for air navigation, i.e. €479.02 per 1,000 litres in 2018.

Features:

Revenue Foregone: Marked Gas Oil for Rail Transport, Water Transport, Agriculture and Industry

Excise duty (including carbon tax) on marked gas oil was €102.28 per 1,000 litres in 2018. Excise duty (including carbon tax) on petrol was €587.71 per 1,000 litres. The revenue foregone by the State due to the reduced tax rate on marked gas oil compared with a benchmark or reference rate of the excise duty on petrol is calculated as the difference in the rates multiplied by the volume of marked gas oil purchased. This method does not account for the possible reduction in purchases of marked gas oil if the excise duty were higher, but assumes that the volume of purchases remains constant. Marked gas oil used for heating is excluded from this calculation.

Partial Excise Repayment on Aviation Gasoline used for Commercial Purposes

Aviation gasoline that has been used for a commercial or business purpose is subject to a refund at a rate of €232.27 per 1,000 litres.

Marine Diesel Scheme

This scheme is a repayment of VAT paid on marked gas oil, marked kerosene, or fuel oil used for combustion in the engine of a registered, qualifying sea-fishing vessel.

Zero VAT on jet Kerosene for International Flights

Estimates of the tax expenditure due to the zero rate of VAT on jet kerosene for international commercial flights are not available. However preliminary work suggests that this tax expenditure is likely to have cost the State in the region of €100 million in 2018.

Fuel Oil Excise Exemption for Manufacture of Alumina

This is a tax exemption for fuel oil used to manufacture alumina. The figures are estimated using the volume of heavy oil for alumina manufacture and residual fuel oil published by Revenue, with excise charged at a rate of €13.45 per 1,000 litres from 2000-2004, and €14.78 per 1,000 litres from 2005-2017.

Fuel Excise Repayment for Horticulture

This is partial repayment of mineral oil tax paid on heavy oil (diesel, kerosene and fuel oil) and liquefied petroleum gas (LPG) used in horticultural production and in the cultivation of mushrooms.

Revenue Foregone: Fuel Oil

Excise duty (including carbon tax) on fuel oil was €76.53 per 1,000 litres in 2018. Excise duty (including carbon tax) on petrol was €587.71 per 1,000 litres. The revenue foregone by the State due to the reduced tax rate on fuel oil compared with a benchmark or reference rate of the excise duty on fuel used for transport/industry is calculated as the difference in the rates multiplied by the volume of fuel oil purchased. This method does not account for the possible reduction in purchases of fuel oil if the excise duty were higher, but assumes that the volume of purchases remains constant.

Natural Gas Carbon Tax Exemption for Certain Industrial Uses

Relief for Increase in Carbon Tax on Farm Diesel

Free Allocation of Emissions Allowances to Companies within EU-ETS

The EU Emissions Trading Scheme commenced in 2005. Airline operators were included from 2012. An emission permit allows the holder to emit one tonne of carbon dioxide. Major emitters of greenhouse gases were provided with free allowances of emission permits. The revenue foregone due to the free allocation of emission permits is calculated as the annual free allocation multiplied by the average price of a permit at auction.

Electricity Allowance

The electricity allowance is part of the Household Benefits Package, which is available to all householders over 70 and to householders under 70 in certain circumstances. Electricity is generated from a mix of fossil and renewable resources, therefore a proportion of the electricity allowance equivalent to the proportion of electricity generated from renewable sources has been removed from each annual amount.

Electricity Excise Exemption for Domestic Use

This is a tax exemption for household electricity consumption. The figures are estimated using SEAI figures on residential electricity use, with excise charged at a rate of €1.00 per MWh (Megawatt-hour), the rate applied to electricity use by non-business users in 2018.

The subsidy is pro-rated by the proportion of electricity generated from fossil as opposed to renewable sources.

Revenue Foregone: Business Electricity Use

This was a reduced excise rate for business electricity consumption compared with non-business consumption. The figures are estimated using SEAI figures on business electricity use, with excise charged at a rate of €1.00 per MWh (Megawatt-hour), the rate applied to electricity use by non-business users in 2018.

The subsidy is pro-rated by the proportion of electricity generated from fossil as opposed to renewable sources.

Relief from Taxation on Electricity used for Certain Industrial Purposes

Relief from Taxation on Electricity generated in Certain Circumstances

Gas, Fuel, Heating and Smokeless Coal Allowances

The gas allowance is part of the Household Benefits Package, which is available to all householders over 70 and to householders under 70 in certain circumstances. The fuel allowance is a social welfare payment to households. It is a means-tested subsidy towards the cost of fuel with the objective of preventing fuel poverty. A coefficient of 0.4 is applied to the heating supplement to take account of the fact that it is only partly used to support households with their heating costs. This coefficient is also applied to the fuel allowance to account for purchases of wood and for other non-fossil fuel purchases. The smokeless coal allowance was paid to low-income households to help them meet the extra costs of using smokeless or low smoke fuels.

Revenue Foregone: Kerosene

Excise duty (including carbon tax) on kerosene was €50.73 per 1,000 litres in 2018. Excise duty (including carbon tax) on marked gas oil was €102.28 per 1,000 litres. The revenue foregone by the State due to the reduced tax rate on kerosene compared with a benchmark or reference rate of the excise duty on fuels used for heating is calculated as the difference in the rates multiplied by the volume of kerosene purchased. This method does not account for the possible reduction in purchases of kerosene if the excise duty were higher, but assumes that the volume of purchases remains constant.

Revenue Foregone: Non-auto LPG

Excise duty (including carbon tax) on non-auto LPG was €32.86 per 1,000 litres in 2018. Excise duty (including carbon tax) on marked gas oil was €102.28 per 1,000 litres. The revenue foregone by the State due to the reduced tax rate on non-auto LPG compared with a benchmark or reference rate of the excise duty on fuels used for heating is calculated as the difference in the rates multiplied by the volume of non-auto LPG purchased. This method does not account for the possible reduction in purchases of non-auto LPG if the excise duty were higher, but assumes that the volume of purchases remains constant.

Zero Excise Duty on Natural Gas

Solid Fuel Carbon Tax Exemption under Diplomatic Arrangements

Reduced VAT rate on Energy Products

Transport subsidies often indirectly increase carbon dioxide emissions from fossil fuel combustion. They are included here for reference.

Road Haulage Development Programme

This programme was run until 2009 by the Department of Transport.

PSO Air Services Scheme

Air services from two airports in Ireland are currently supported by this scheme, on the basis that these services are considered necessary for the economic development of their regions and that they would not be provided on a commercial basis. Current contracts are in place for air services between Dublin and the regional airports in Kerry and Donegal. Previously the scheme supported six regional airports.

VAT Relief for Touring Coaches

Operators involved in the transport of tourists by road under a group contract may reclaim Value Added Tax (VAT) incurred on the purchase, intra-Community acquisition, lease or hire of touring coaches.

VRT Relief for Leased Cars

A partial repayment of VRT was available since 1993 on certain vehicles acquired by vehicle leasing or hiring businesses or for providing driving lessons. The repayment is not be available for vehicles registered on or after 1 January 2019.

VRT Exemptions

Under certain conditions, VRT exemptions can be applied to the vehicles of a business moving permanently to Ireland from abroad, an inherited vehicle, a donated vehicle, diplomatic vehicles, vehicles belonging to EU institutions, and vehicles used to support international air services.

Repayments of VRT: Disabled Drivers and Disabled Passengers Scheme

A remission or repayment of VRT may be claimed by a driver with a primary medical certificate (PMC), a passenger who has a PMC, a family member residing with, or responsible for the transportation of a passenger who has a PMC, or a registered charity engaged in the transport of persons who have PMCs whose purpose is to provide services to persons with disabilities.

Multi-storey Car Parks

This was a scheme offering tax relief on the construction or refurbishment of multi-storey car parks. It ran from 1995 until 2008. The final year of repayments is 2021.

VAT Rate of 0% on International Flights

Airline tickets are not subject to VAT.

Special Marketing Fund for Regional Airports

A figure of €1.905 million is available for the year 2000 only.

Removal of Air Travel Tax

The cost of this tax expenditure was estimated as €51.8 million in 2017. However the air travel tax is usually used as an alternative to a tax on aviation fuel and the tax expenditure on jet kerosene has already been included in this release.

Hide Background Notes

Hide Background Notes

Scan the QR code below to view this release online or go to

http://www.cso.ie/en/releasesandpublications/er/ffes/fossilfuelsubsidies2018/

Show Table 1: Average Effective Carbon Rate by Sector and Fuel, 2000-2018

Show Table 1: Average Effective Carbon Rate by Sector and Fuel, 2000-2018 Hide Table 1: Average Effective Carbon Rate by Sector and Fuel, 2000-2018

Hide Table 1: Average Effective Carbon Rate by Sector and Fuel, 2000-2018